Disclaimer: I am not a registered investment advisor and do not have the qualifications to become one. Even if I was one, I would not be your investment advisor; to you, I am nothing more than a random guy on the Internet writing in his personal blog. This content is intended for comedic and entertainment purposes only. Everyone’s situation is uniquely different, so consult a certified professional if you need guidance with your own financial strategy.

A few days ago, my friend Doug Wreden, a broadcast personality who streams on Twitch and makes video content on YouTube, asked if I wanted to join in on a live event he was doing with his community where, together, they would invest $10,000 into the stock market. Unfortunately, I was overloaded with time-sensitive work that entire day and couldn’t join in live, but we decided to do the next best thing, which was for me to participate after-the-fact.

Thus, “Parkzer vs. DougDoug’s Twitch chat” was born.

Rules:

- Invest US$10,000.00 into ten individual companies (no index funds, mutual funds, ETFs, or bonds).

- No active trading is permitted after the initial purchase (though reinvesting dividends is allowed), and stocks must be held for one year.

- The winner is the team with the highest account balance after one year.

- Any profits beyond cost basis will be donated to charity.

Doug has very little investing experience (apart from purchasing Dogecoin as a joke and making a +800% return), so he relied on his community’s assistance to research companies and pick out the best stocks. Doug uses Robinhood as his brokerage, so that basically speaks for itself. On the other hand, investing and wealth management is one of my favorite hobbies, and I’ve taken it very seriously ever since my first paying job.

However, I knew I couldn’t let this make me get complacent. There are plenty of studies proving that even monkeys randomly throwing darts on a wall of stock ticker symbols can consistently beat investment advisors. Just because I’ve been doing this for longer doesn’t necessarily mean I am going to perform better by default. I needed to establish a plan.

First, I had to make some predictions and assumptions about what would happen in the coming year. Nobody can predict the future, but what I can do is use current events and cultural trends to make educated guesses. From there, I had to determine which sectors of the market are more and less likely to perform well in the given conditions. Next, I found some companies within those aforementioned sectors that I thought had potential for growth. Finally, I had to trim down my list to ten of my best candidates.

I made three major assumptions upon which I would base my investment decisions:

- I think the coronavirus pandemic will continue through sinusoidal phases of getting better and worse throughout the year. Although the latest variant has not been as deadly, it has evolved to become far more contagious. We don’t know how it will mutate next, and with people getting complacent, this is a ripe opportunity for COVID-19 to cause great damage when we least expect it, resulting in a stock market crash.

- I think it is more likely for the stock market to stabilize or fall than it is to rise in the coming year. I think the current state of the stock market is not as healthy as it may seem—it is only this high due to absurd inflation and government policy stimulating economic growth. Once things return to normal and people start repaying their COVID-19 disaster relief loans, money will be taken out of circulation and the stock market will revert back to what it “should” be.

- I think the development and modernization of core systems will get faster. Technology companies did well the past few years, but it will still require more work to roll out their advancements infrastructurally so it turns from a luxury into something more commonplace. In simpler terms, I think we have a lot of great concepts, prototypes, and first-generation innovations, but now is the time to keep pushing development so it can be used not only by the elite, but also by the general public.

With my grim outlook on the future of the stock market, it is clear that I would have to pick sectors that perform well during a recession. Out of the sectors defined under the Global Industry Classification Standard (GICS), I knew I wanted to focus on the following:

- Consumer staples. No matter how bad the economy, people still need to eat and use core household products. When people have less disposable income, they tend to shift their money away from consumer discretionary and into consumer staples.

- Healthcare. Just because the economy is bad doesn’t mean you’re not going to get sick. On top of that, we are still in the middle of a pandemic caused by a virus that is actively mutating. The healthcare industry is booming, ignoring the fact that that’s probably not the most sensitive way to describe people’s misfortune.

- Utilities. Similar to the above, people still use utilities during a recession, even if they might try to conserve spending and be more conscious of wastefulness.

- Real estate. Again, as you might have guessed, people still need a place to live, even if the economy is bad. However, real estate also bundles in development projects, which ties in with the infrastructural advancements I mentioned above that I think will happen.

I picked three well-established, reputable companies from each of the sectors above, plus three companies from the remaining sectors not listed above. From there, I took the list of 15 and narrowed it down to 10.

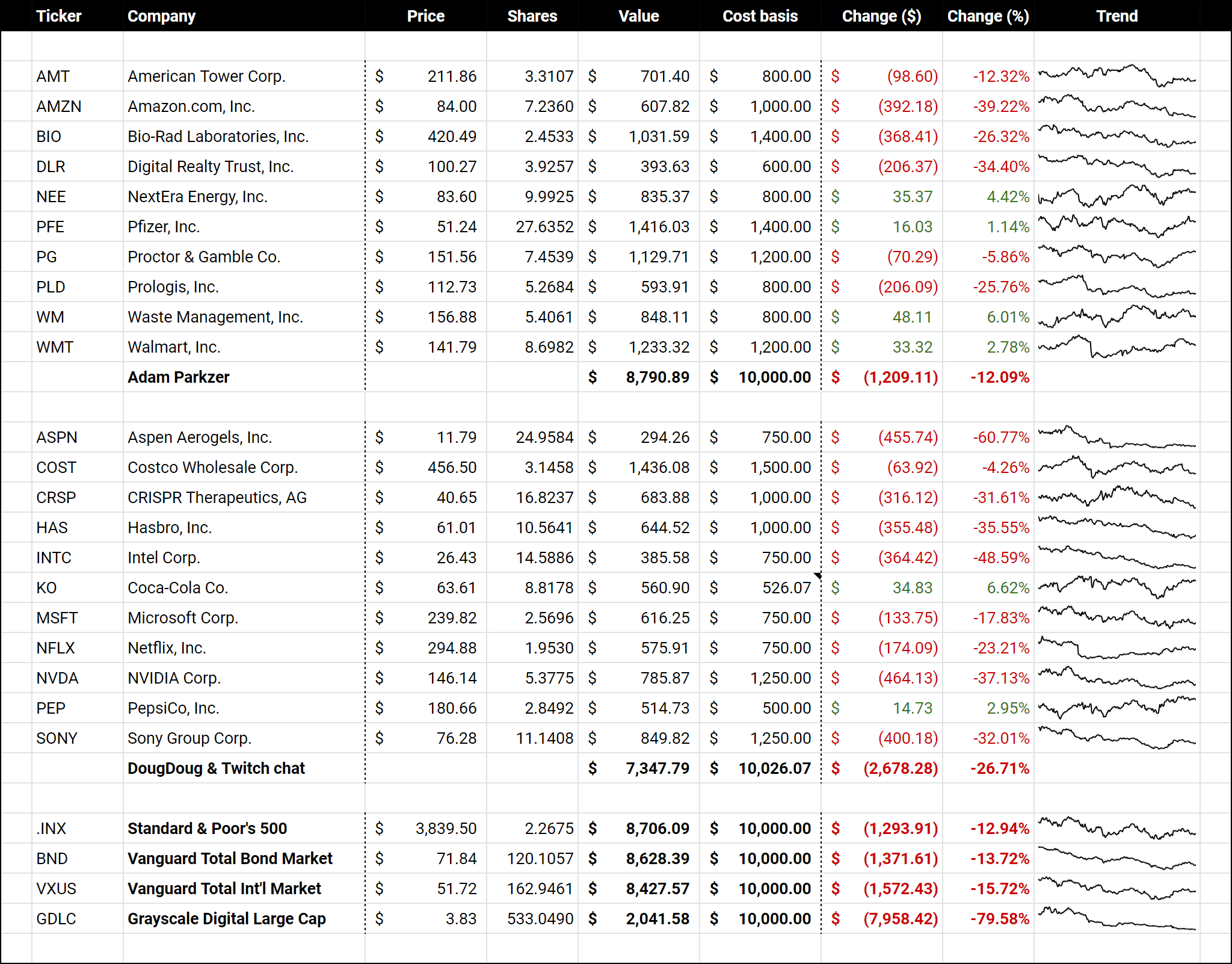

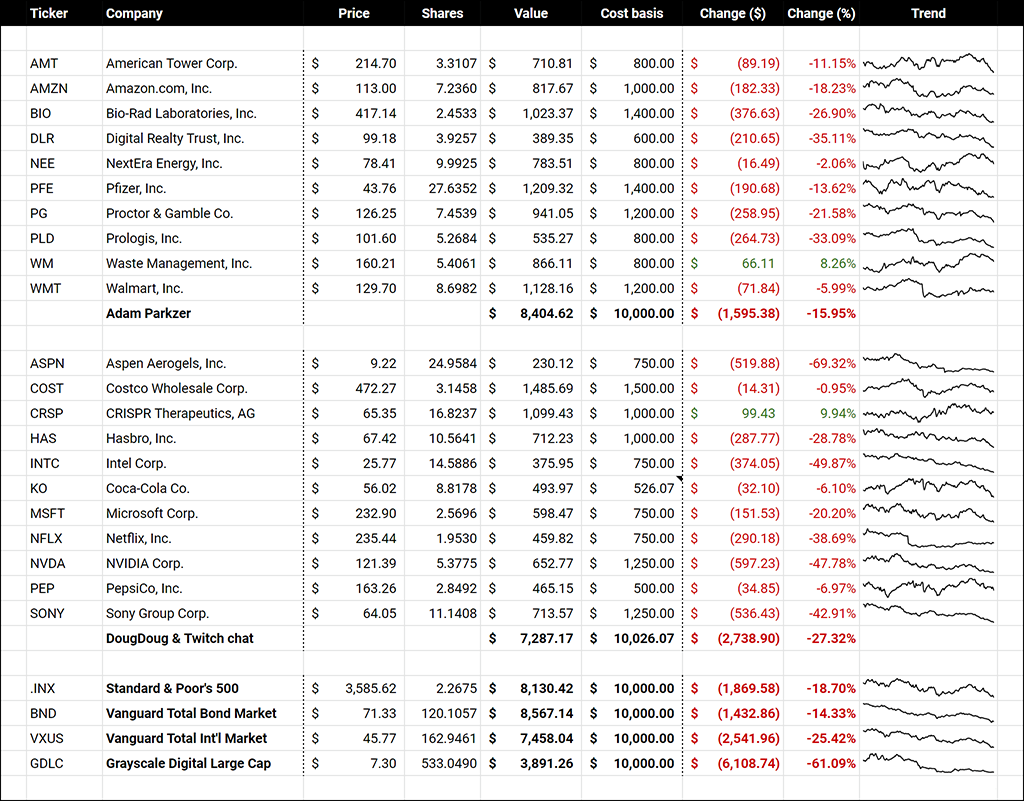

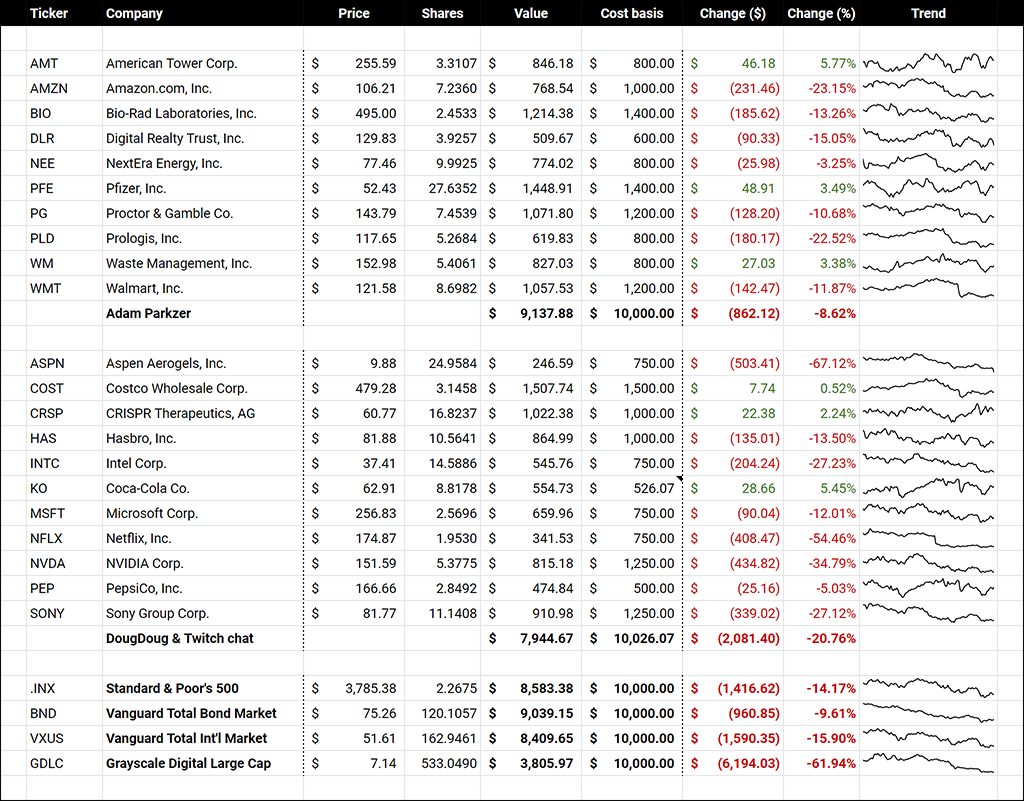

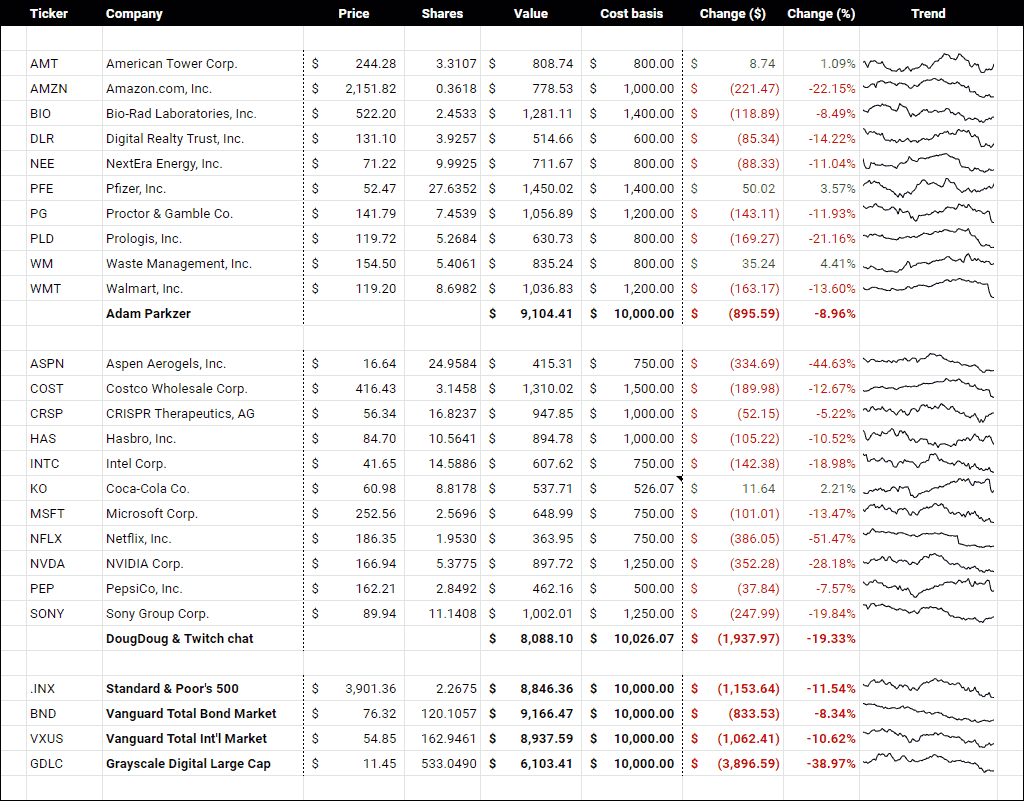

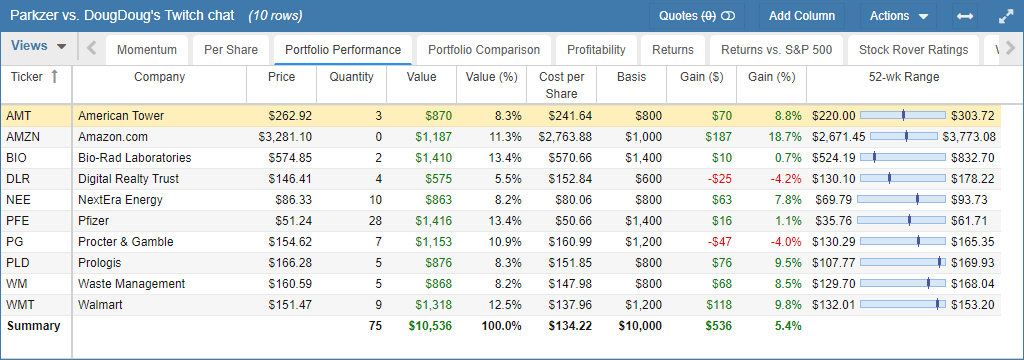

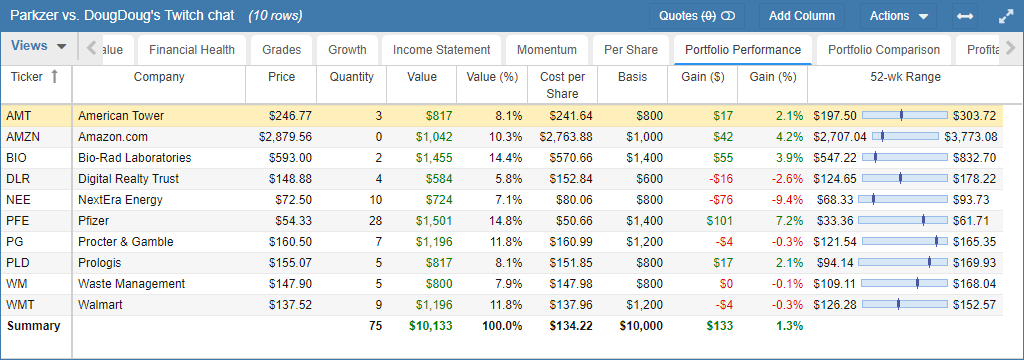

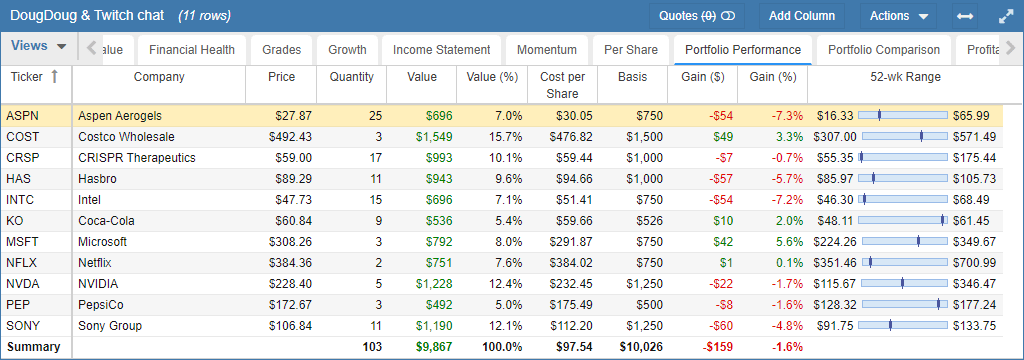

Here are my ten stocks picks with the amount of money I allocated to each company, alongside Doug and his community’s stock picks and their allocations:

NextEra Energy, Inc. (NEE) | $ 800.00 |

Waste Management, Inc. (WM) | $ 800.00 |

Proctor & Gamble Co. (PG) | $ 1,200.00 |

Walmart, Inc. (WMT) | $ 1,200.00 |

Bio-Rad Laboratories, Inc. (BIO) | $ 1,400.00 |

Pfizer, Inc. (PFE) | $ 1,400.00 |

American Tower Corp. (AMT) | $ 800.00 |

Prologis, Inc. (PLD) | $ 800.00 |

Digital Realty Trust, Inc. (DLR) | $ 600.00 |

Amazon.com, Inc. (AMZN) | $ 1,000.00 |

| |

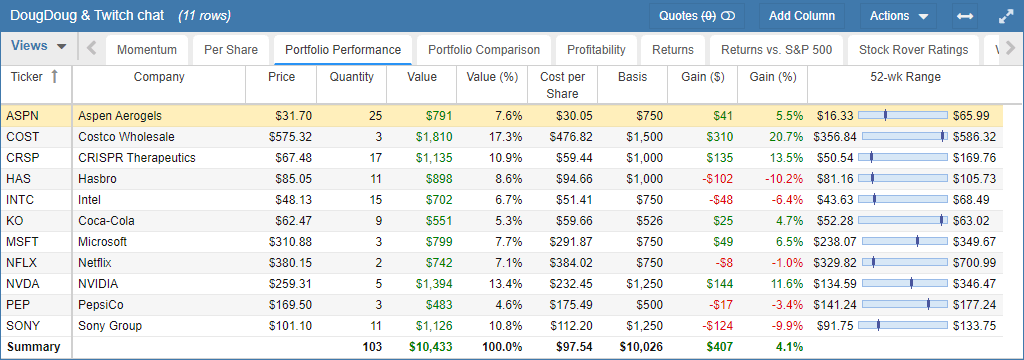

NVIDIA Corp. (NVDA) | $ 1,250.00 |

Aspen Aerogels, Inc. (ASPN) | $ 750.00 |

Sony Group Corp. (SONY) | $ 1,250.00 |

Netflix, Inc. (NFLX) | $ 750.00 |

Intel Corp. (INTC) | $ 750.00 |

CRISPR Therapeutics, AG (CRSP) | $ 1,000.00 |

Hasbro, Inc. (HAS) | $ 1,000.00 |

Microsoft Corp. (MSFT) | $ 750.00 |

Costco Wholesale Corp. (COST) | $ 1,500.00 |

The Coca-Cola Co. (KO)

PepsiCo, Inc. (PEP) | $ 1,000.00* |

|

*The $1000 for Doug’s final stock selection is split evenly between Coca-Cola and Pepsi as a mini-game between “A Crew” and “Z Crew,” two halves of Doug’s Twitch chat community split by the first letter of their username, to see which brand (and consequently, which crew) has a higher return on investment.

From these stock picks, I think it becomes fairly clear that my portfolio was built not to grow faster, but to decline slower. Thus, if the economy continues to do well, Doug’s portfolio will defeat mine, but the economy slows down, my portfolio’s balance will conclude the year higher.

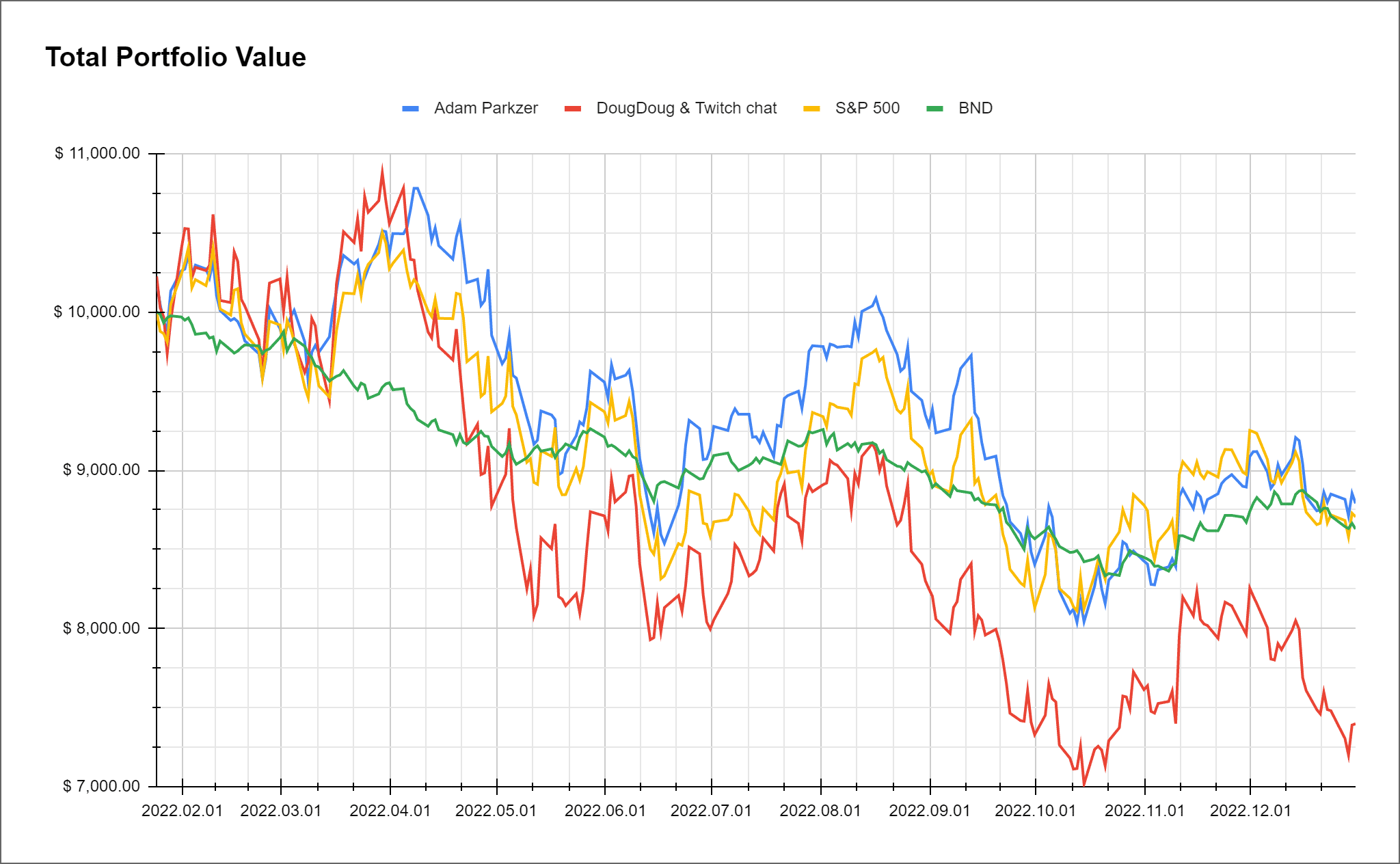

I’ve loaded all of our stock picks into some portfolio analysis software, and I might do quarterly (or even monthly, depending on level of interest) reports on the performance of our portfolios, showing who is in the process of winning. At the very least, I’ll be providing some statistics, charts, and tables for Doug to be able to review on his live stream.

Seeing as this is ultimately going to be for charity, I wish great success for Doug and his Twitch chat… with the caveat that his portfolio yields 1¢ less profit than mine. GL

Edit (January 28, 2022):

It’s been a week since we started this little competition, so I decided to go back and edit this blog post to add in some bonus content in the form of charts and a graph.

First, one thing to note is that, if you’re attentive to the numbers, you’ll notice that Doug’s cost basis is not a flat $10,000.00. This is because, when he was picking out stocks on his Twitch stream, he intended to invest $500 in Coca-Cola (as in, the competitor to Pepsi), but instead, he accidentally invested it into the Coca-Cola Bottling Co. Consolidated. This happened because the bottling company’s ticker symbol is COKE, while the Coca-Cola Company’s ticker symbol is KO; Doug and his Twitch chat got those two mixed up.

After I informed Doug of this error, he sold all his shares of COKE and realized $26 in profit, then put all $526 into KO. I was not aware that he was going to do this, otherwise I would have advised him to only put $500.04 back into KO, because that would’ve been the equivalent return on investment from KO from that time period. Thus, because of the transaction, Doug’s numbers are going to be a little bit off.

Hopefully the final results won’t come down to $26, but if our portfolios are indeed within $26 of each other at the end of one year when we determine the winner, we’re going to need to do a bit of math to see how much this affected Doug’s earnings.

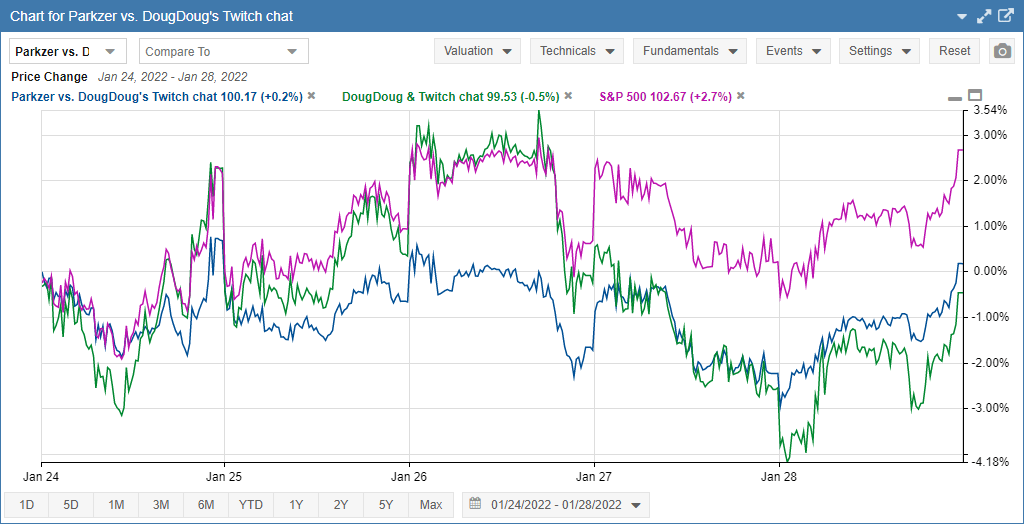

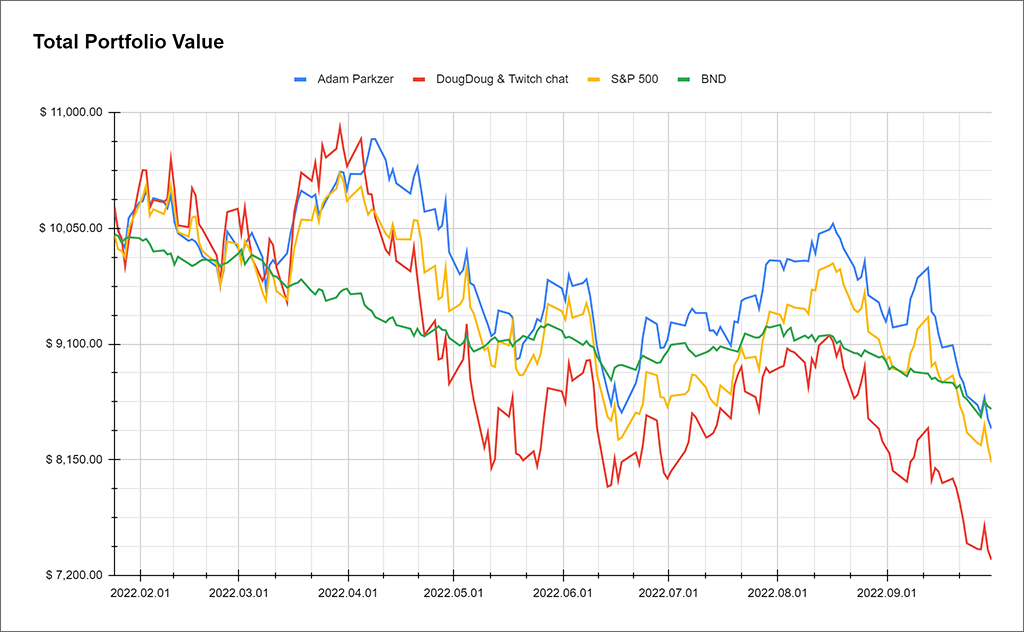

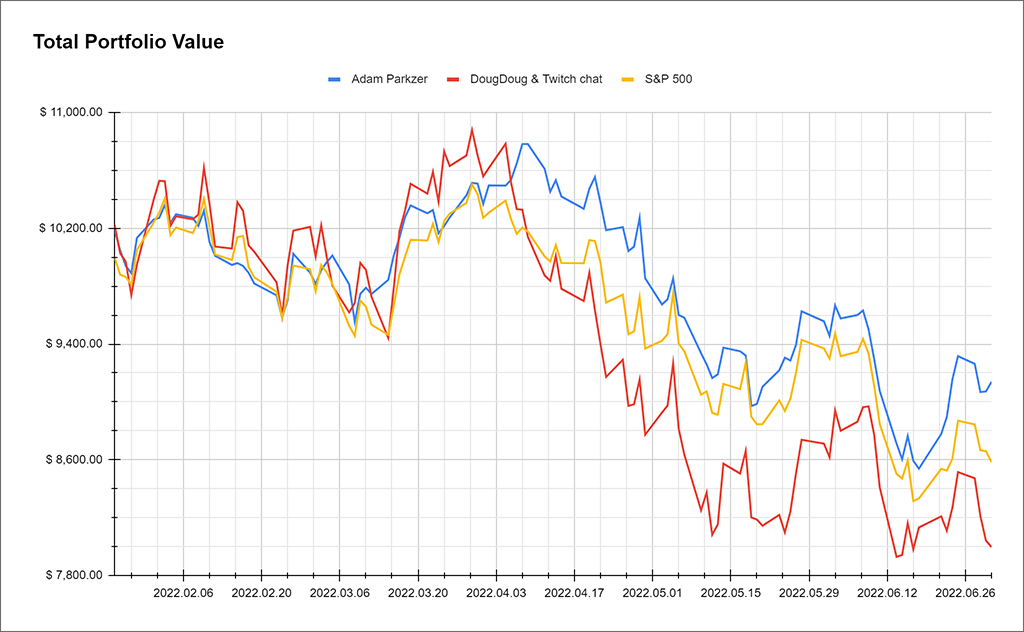

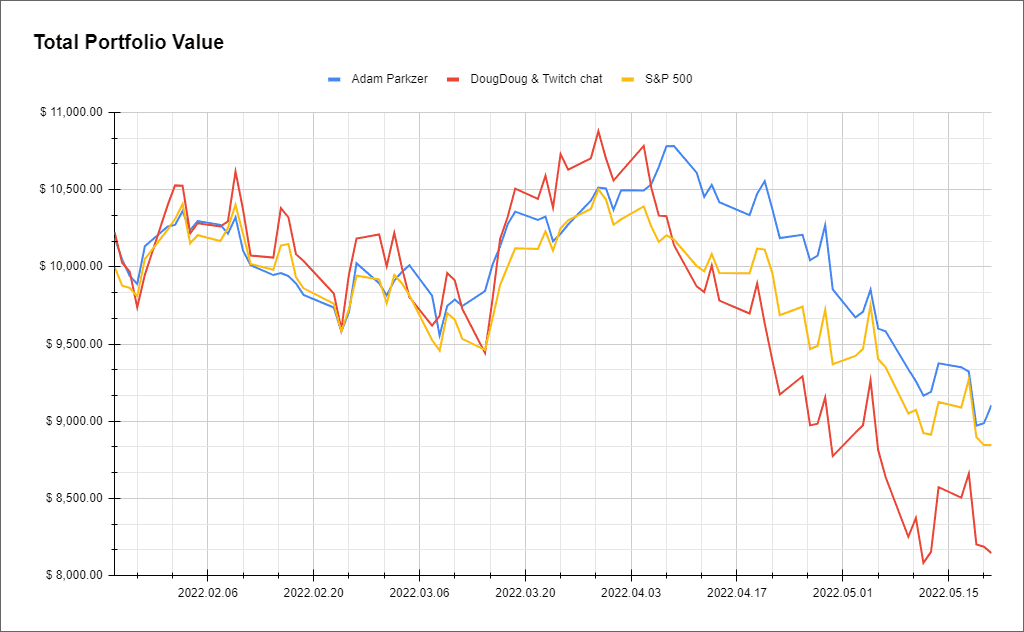

After five market days, this is how our portfolios are looking right now:

For comparison, if we had invested the $10,000 into the S&P 500 instead, it would have grown to $10,230—$97 higher than my portfolio, and $363 higher than Doug’s.

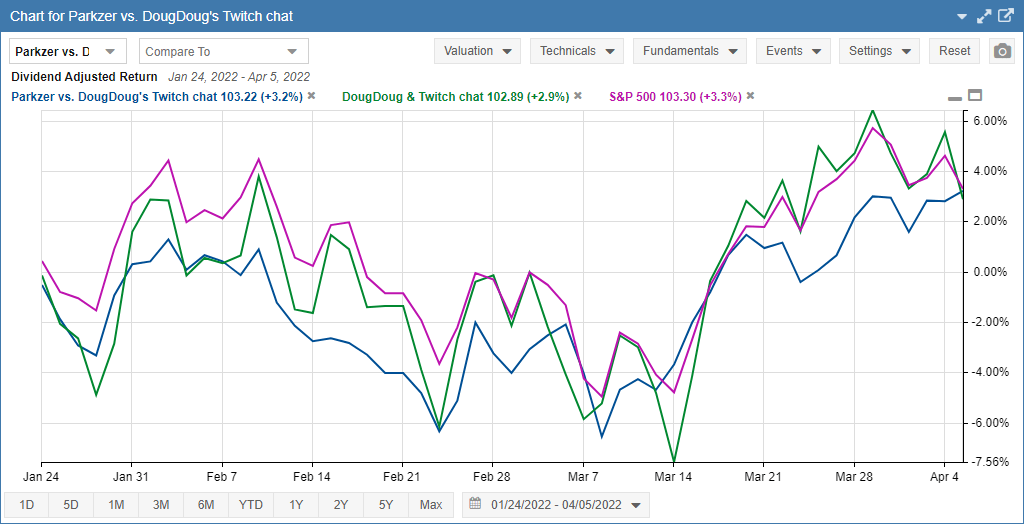

Here is a graph of the price change of each of our portfolios, alongside the chart for the S&P 500. Keep in mind that these are by percentage, and are relative values, so this might not be the most intuitive graph. I ideally would have wanted to graph the total value of each of our portfolios over time in dollar amounts, but it seems like that is not a feature offered by my portfolio tracking and analysis software.