Happy April Fool’s Day—that means it’s time for another investment allocation breakdown. Yes, all of the information in this breakdown is accurate; no, there are no April Fool’s jokes in these numbers.

As of last month, it has been one full year since I’ve done investment breakdowns. Out of all the quarter-over-quarter breakdowns, I think the first quarter of the year is going to be the most interesting with the greatest number of changes, because the beginning of the year is naturally the time when I spend the most cash on investments, considering that calendar-year restrictions obviously refresh on January 1.

Keep in mind that this is a series, and I’m trying not to repeat information post-over-post, so you may not be able to get a complete picture of my investment portfolio unless you go back and read the previous installments.

And of course, like usual, a disclaimer: I am not a registered investment advisor, and even if I was, I wouldn’t be your investment advisor; to you, I am nothing more than a blogger on the Internet writing personal anecdotes on his website. I am in no way suggesting or implying that you should copy my strategy; everyone’s situation is uniquely different, so you should consult and hire a certified professional if you need guidance with your own financial planning.

Cash As expected, my cash balance has had the most significant decline from the previous quarter, as I’ve used a large portion of it to buy investments during January. I personally think that, if you don’t have a clear plan for your cash balance, then you should hold as little cash as possible; the allocation I have towards cash right now (as opposed to previous quarters) is a lot closer to what I think is reasonable and ideal for my situation. | 5.84% |

Domestic total market index funds Very few changes here—this is approximately the same amount of money as last quarter (minus the market changes, obviously), with the exception of purchasing additional shares of FZROX via a maximum 2022 contribution to my Health Savings Account. | 26.08% |

International total market index funds There are no changes to my international index fund allocation, except for the fact that the international market has been the worst-performing holding in my portfolio for a while now. I’m not discouraged, though; this may be a decent opportunity to buy more while it’s low. | 7.37% |

Target retirement funds As the “set it and forget it” segment of my portfolio, I had a noticeable jump in target retirement funds because I maxed out my 2022 Roth IRA contribution, put a large chunk into my 2022 SEP-IRA, and rounded out my 2021 SEP-IRA contribution after doing my taxes and calculating the exact tax-year limit. As a reminder, I categorize this separately because target retirement funds are self-adapting in composition. If you’re curious what mine specifically are made of, I generally split my contributions almost evenly between VFFVX and VTTSX. | 24.75% |

Real estate investment trusts (REITs) No changes. | 16.45% |

Bonds I went into far greater detail about this in a recent finance blog post about investing US$10,000 into individual companies as a competition with my friend Doug Wreden, but I personally do not think the stock market is going to do well over the next year. Because of this, I’m more willing to turtle up with bonds and other safer investments. I added onto my bond balance again this quarter, and will most likely hold onto them until the next recession cycle is over, at which point I will exchange them for higher-risk investments again. | 8.17% |

Precious metals Following a similar spirit as the above, I invested in precious metals for the first time in my life this quarter. I did some light research about them, and although I still don’t really understand the nuances of metals investments yet, I still figured it’s a good way to diversify my portfolio. I do a majority of my investing with Vanguard, but I have a Fidelity account for the things that Vanguard doesn’t offer—namely, a Health Savings Account and a Charitable Giving Account. A good precious metals fund also appears to be something Vanguard doesn’t offer (the Global Capital Cycles Fund seems to be the closest thing, but that only invests about a quarter of its funds into precious metals), so I decided to use my previously-dormant individual brokerage account under my Fidelity profile to purchase FSAGX. | 2.00% |

Cryptocurrency The best thing about my cryptocurrency investment so far is the fact that I was able to use it for maximum tax loss harvesting in 2021. Apart from that, I’m just holding onto it, terrified to buy more in case it keeps crashing, but also concerned that “cutting my losses” now will result in cryptocurrency rebounding and becoming mainstream and running away with all my potential profit. | 6.99% |

Speculative stocks and individual companies I decided to purchase some more individual securities, namely in Cloudflare and T-Mobile, both companies that I believe in and have personally been using for a while now. There were some dips in the prices of both stocks over the past quarter, so I took advantage of that opportunity and grabbed some shares on sale. | 2.35% |

Notably missing from this breakdown, like usual, is my equity ownership of Tempo, as revealing that would likely heavily skew percentages and also potentially implicitly reveal some of the company’s confidential information.

Another thing that is missing here is the $10k I spent on stocks in the competition with Doug, the blog post for which I linked above in the “Bonds” section. I don’t have a particular reason for not including it—I just happened to forget about it, as I have those stocks held in a separate account, and it takes a lot of work to add together all the numbers and calculate percentages, so I didn’t want to bother redoing all the work… heh.

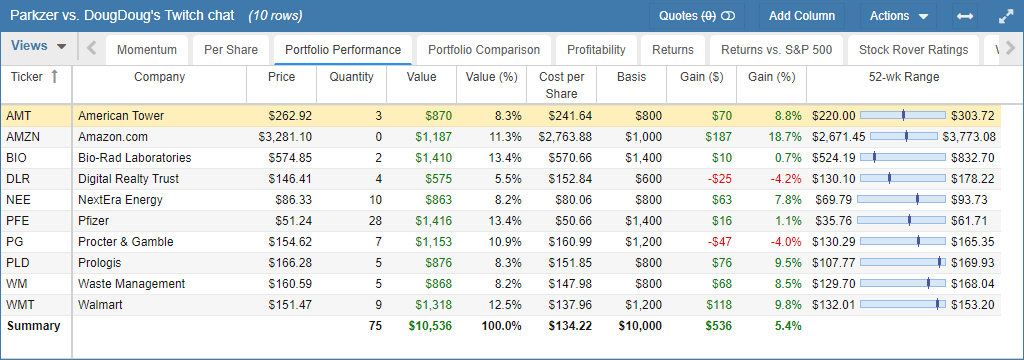

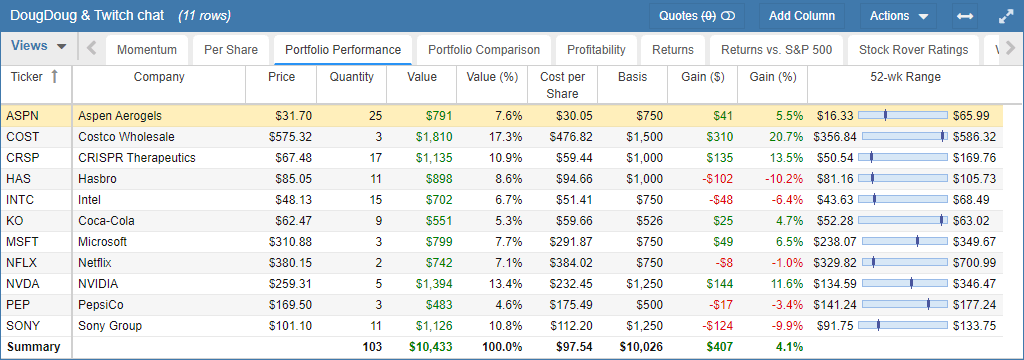

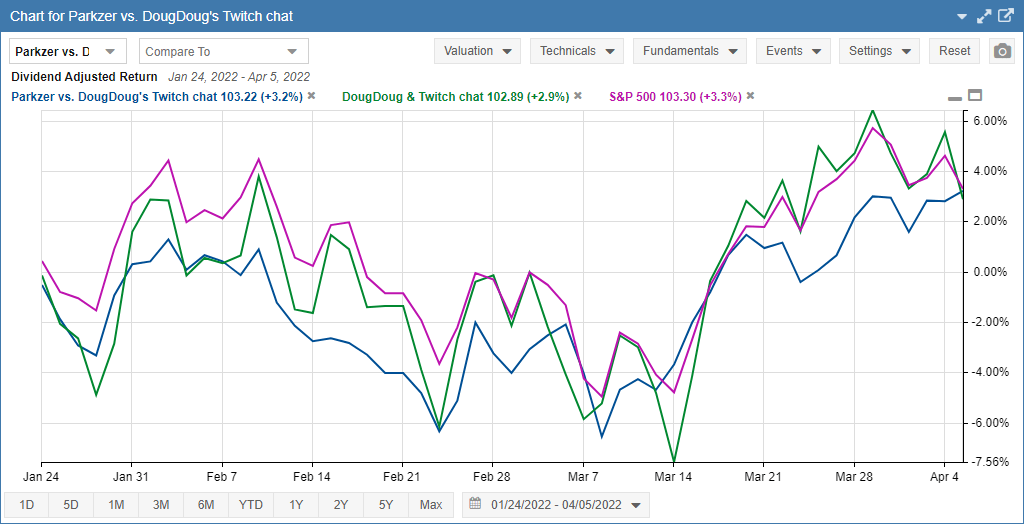

Speaking of the competition with Doug, I haven’t posted an update about our progress since a week after we did the initial stock purchases, so I decided to edit this blog post and throw in some tables and a chart to show how our picks were doing.

As of the end of the market trading day today, my portfolio is valued at $10,536 and Doug’s portfolio is valued at $10,433. For comparison, if we had invested into an S&P 500 broad index fund instead, the portfolio would be worth $10,441.

One thing to keep in mind here is that the stock market is fairly volatile right now, and with our portfolios having only ten and eleven companies, there can be huge fluctuations in a matter of days. In fact, I’d say it’s mostly luck that I happen to have the highest portfolio balance today; for a good chunk of the past month or so, it was Doug whose portfolio value was beating not only me, but the S&P 500 as well.