Disclaimer: I am not a registered investment advisor, nor do I have the proper qualifications to become one. The information contained in this blog post is intended to be strictly anecdotal as a means of personal storytelling, and it should not be construed as financial advice. Everyone’s situation is uniquely different, so do not blindly copy my strategy; instead, consult with a certified professional if you have any questions or need proper guidance.

After doing these investment breakdowns quarterly for over a year now, and each quarter, building upon the previous quarter’s breakdown, I realized that it’s not very realistic to ask people to go down the entire rabbit hole of all of my past investment allocation breakdowns in order to understand the full context of anything new that I’m sharing. Because of this, I have decided to do a “comprehensive edition” of my investment breakdown at least once a year in order to “reset” the trail of breadcrumbs and provide a new standalone anchor point from which readers can start.

Because of this, this particular comprehensive edition of 2022 Q2’s investment allocation breakdown is going to be a lot more detailed and will contain lots of repeated information from previous posts—which is the entire idea here, as the main point of me doing this is to be able to compact everything important into a single article so readers won’t have to navigate back in time.

Now, with that having been just said, I think this may seem pretty silly, but I direct you to a blog post that I published in the past titled “Investing US$10,000.00 in the stock market – Parkzer vs. DougDoug’s Twitch chat.” In that post, I discuss my current outlook on the market; it will give a general explanation as to why I seem to be so focused lately (within the past half a year or so) with portfolio diversification and alternative investment classes.

Cash I subscribe to many safe-investing principles, including the idea that time in the market is better than timing the market, and how you should always hold minimal cash—only enough to cover your emergency fund. If anything makes you heed my disclaimer above about how I’m not an investment advisor, it should be this—I am at an all-time high in cash holdings, and I am being a hypocrite and not following my own advice. I didn’t recently sell investments in preparation for making a major purchase or anything—I just don’t feel comfortable dumping a bunch of money into the stock market right now until I see some modicum of stability return to the charts. I am losing a substantial amount of value from my money due to high inflation by just holding it in cash, but that is a trade-off I’m wiling to accept to avoid losing even more to a crashing market. My bank account of choice is the Discover Online Savings Account. I’ve been a Discover customer ever since I was 18 years old and got my first credit card; Discover has always been reliable for me, and because it is an online bank, even though the interest rate on the savings account is tiny, it is still astronomical compared to traditional brick-and-mortar banks that may offer less than a tenth (or even a hundredth) of a percentage point. | 27.19% |

Domestic broad market index funds For the money that I do still have in the stock market, a large portion of it is in domestic broad market index funds, namely Vanguard Total Stock Market Index Fund Admiral Shares (VTSAX) and Vanguard High Dividend Yield Index Fund Admiral Shares (VHYAX). I use Vanguard as my primary brokerage, but I also have a Fidelity account for account types that Vanguard doesn’t offer—namely a Health Savings Account and a regular brokerage account that supports incoming transactions of over-the-counter securities (which Vanguard recently stopped supporting in late April) (I also hold my 529 College Savings Plan with Fidelity because the sign-up process was much easier than Vanguard’s). Within my Fidelity HSA, I hold my money in the form of the Fidelity ZERO® Total Market Index Fund (FZROX). Although I’m hesitant in current market conditions, domestic broad market index funds are my favorite category of investment. Each calendar year when limits reset, I max out my tax-advantaged accounts, and all other investments into the stock market generally go into brokerage accounts in the form of broad market index funds. | 17.84% |

International total market index funds For the purpose of diversifying outside of the United States of America, I also own Vanguard Total International Stock Index Fund Admiral Shares (VTIAX). I don’t know much about countries outside the United States, and I am probably grossly uneducated about international matters, but I know for a fact that the United States is not the only successful country in the world, and I want to make sure that I have exposure to outside markets in case something horrible happens to the United States and/or something incredible happens to a foreign country. Beyond that, I don’t really have much further insight here; I just picked out a broad market index fund specifically focusing on non-US companies (as opposed to worldwide index funds) such that I don’t have any overlap with domestic index funds I already own, and can control and proportion my exposure to global markets. | 5.29% |

Target date funds In my retirement accounts, specifically my Roth IRA and SEP-IRA, I like to purchase target-date broad-market index funds. Specifically, I have my money split fairly evenly between Vanguard Target Retirement 2055 Fund (VFFVX) and Vanguard Target Retirement 2060 Fund (VTTSX). The premise of a target date fund is to pick out a year in the future for when you think you are going to need to start making withdrawals, and the index fund manager automatically adjusts the holdings of the fund to optimize growth up until that point. For example, if you are expecting to retire in 2060, these funds will invest heavily in high-risk, high-return stocks for now, but as it gets closer to 2060, the fund will progressively shift holdings into low-risk, low-return bonds such that your money won’t suddenly plummet if a stock market crash were to happen close to your retirement year when you need to start making withdrawals. Due to annual contribution limits set by the government on these tax-advantaged retirement accounts, a majority of my investments are in regular brokerage accounts. Thus, by putting all my tax-advantaged retirement savings into target date funds, I’m only putting a relatively small percentage of my investment into these automatically-adjusting portfolios, and I am manually managing everything else outside of these retirement accounts. A reasonable question I often get is why I don’t manually self-manage all of my investments (including retirement savings), instead of entrusting my IRA contributions to Vanguard’s fund manager, considering how involved I already am with investing and wealth management. The main reason is so it can act as a safeguard in case something happens to me in the future where I am no longer able to actively manage my own money. Of course, I imagine that the likelihood of that actually happening (and then my caretaker also not being able to actively manage my money) is inconceivably low. However, for my personal risk tolerance, I feel like I already have plenty of other investments such that I’m willing to sacrifice a bit of money on an automatically-managed target date fund with a slightly higher expense ratio so it acts like a makeshift insurance policy for my retirement, in case the market crashes right when I need the money. As a side note, I also recently started taking advantage of another tax-advantaged account, the UNIQUE 529 College Investing Plan. I set one up with Fidelity, and again, for the sake of convenience, and because of how small of a fraction of my total portfolio this accounts for, I was comfortable just putting the money into a target date fund. Based on the fact that I may use this money myself for further education (as opposed to passing it onto my children), Fidelity selected the NH College Portfolio (Fidelity Index) as my fund. | 20.53% |

Real estate investment trusts (REITs) If you ask people how to best diversify your investment portfolio, the go-to answer from most people is usually going to be real estate. Unfortunately, traditional real estate has a relatively high barrier of entry—not only do you have to go out and find a physical property at a reasonable price with good potential for positive cash flow, but you also need to put a chunk of capital down to purchase the property, even if you’re loaning money from a lender. Luckily, there are some alternatives for real estate investment that don’t involve purchasing an actual building, facility, or plot of land. The real estate investment trust is an investment vehicle that allows you to invest in a company that, to put it simply, acts like a landlord on your behalf and shares their real estate profits with you. A vast majority of taxable revenue from income-driving activities, such as collecting rent payments from leasees, are distributed to REIT shareholders in the form of dividends. Because I personally am not at a point where I feel ready to commit to purchasing physical real estate, 100% of my real estate investment exposure is through Vanguard Real Estate Index Fund Admiral Shares (VGSLX). | 11.72% |

Bonds I have been relatively fickle with bond holdings because of how young I am and how much opportunity cost there is to investing in bonds instead of in stocks, considering the amount of runway I have prior to needing to withdraw from my investments. With that being said, upon the full onset of the COVID-19 pandemic and the relief efforts the United States government took to print an absurd amount of money out of nowhere, it was fairly obvious that inflation was going to skyrocket. This was less well-known before, but I’m glad that this information is much more commonplace now—the United States Department of the Treasury offers a special bond called the Series I Savings Bonds that acts as a hedge against inflation. As of this writing, the interest rate on these bonds is 9.62%, which is earth-shatteringly high considering that many people are losing double-digit percentages on their portfolios by investing their money elsewhere. An overwhelming majority of my bond holdings are in the form of Series I Savings Bonds. It’s a great way for me to retain as much of my money’s existing value as possible for now, and then once the market stabilizes, I can sell the bonds and reallocate them back into higher-risk stocks. | 6.77% |

Cryptocurrency I started investing in cryptocurrency primarily as a way to diversify my portfolio, but part of my interest also came from the fact that I saw many other people getting rich off buying into cryptocurrency early, and I wanted to join in on the gamble. Tempo Games is going to be integrating blockchain technology into one of its upcoming game releases. Even though I oversee corporate operations and am not directly involved in game design or technical engineering, I still felt like it would be important for me to be familiar with the concept. One of the best ways to learn is to accrue experience through first-hand, hands-on exposure and experimentation, so I have been making active cryptocurrency investments a lot more in the past few years. I own a decent chunk of Bitcoin and a little bit of Dogecoin and Shiba Inu token, but a majority of my holdings are actually in the form of the Grayscale® Digital Large Cap Fund (GDLC) and the Bitwise 10 Crypto Index Fund (BITW). These are over-the-counter securities that represent underlying cryptocurrency holdings held by the firms and packaged into a single share, the convenience of which is paid for via a 2.5% annual management fee. There are three distinct reasons why I own most of my cryptocurrency in this form:

| 2.87% |

Individual stocks and private companies I went through a phase when I was younger when I was very interested in researching companies and picking out stocks. In the past few years, I was also a participant of the retail investor movement and buying meme stocks. Since then, I’ve waned down my individual company holdings substantially, and instead just stick with companies that are meaningful to me. I own Marriott International, Inc. (MAR) because they have functionally been my landlord for over a year now after I transferred out the lease to my condo in Las Vegas and traveled across the United States and Canada. I am an Ambassador Elite in their loyalty program, which is the highest tier achievable through their Bonvoy system; throughout this incredible volume of travel, as well as additional research I’ve done on other hotel chains, I believe Marriott takes the best approach to lodging out of all the major brands. I also own Cloudflare, Inc. (NET) and T-Mobile US, Inc. (TMUS) because they are two of my favorite companies to work with. I use almost all of Cloudflare’s available services to support my website, and also used them for Tempo’s corporate needs as well, up until we hired a new IT team and they took over that aspect of the company. I’ve been with T-Mobile ever since I left my parents’ AT&T family plan. I have never faced a single problem with either of these companies. In my opinion, both of these companies take an uncommon approach to business, in that they prioritize quality products and high customer satisfaction above anything else, and depend on those two aspects to naturally improve cash flow. Finally, I purchased a nice batch of Stellantis, NV (STLA), the company behind my favorite auto brand and pickup truck, the Ram 1500 Rebel, as well as some other auto companies I’m a fan of, like Alfa Romeo, Maserati, and Jeep. Stellantis has shown great acumen towards advancing vehicle technology and implementing it in previously unestablished ways. I’m looking forward to seeing the Ram all-electric pickup truck, and there is a high chance that it is the next pickup truck that I’m going to end up purchasing. Note that my holdings for the $10,000 investing challenge with DougDoug are not included in this line item (or in this investment allocation percentage breakdown at all), as I consider that more of a special project, and also want to avoid people trying to reverse engineer numbers to calculate my net worth. Instead, I have a brief section about the investment challenge at the end of this blog post. | 4.71% |

Precious metals As a way to even further diversify my portfolio, I took the recently-falling stock market trend as an opportunity to buy into some gold. I’m not really in a position right now to purchase solid gold bars and store them safely with me as a physical hedge against the market, but I found the Fidelity® Select Gold Portfolio (FSAGX) that I can buy from my existing Fidelity brokerage account, which comes close enough. One thing to note here is that I’m not investing in gold because I’m particularly passionate about it or know what I’m doing; this is mostly a “why not” scenario where I am putting in a tiny fraction of my portfolio into something that I’ve always heard could be useful to have during market turbulence. | 1.20% |

Fine art, and other collectibles And finally, as a way to really diversify my portfolio, I began investing in fine art and other collectibles this quarter, and will continue doing so in increments in the future. There were three factors that set me over the “tipping point” to begin investing in fine art:

| 1.88% |

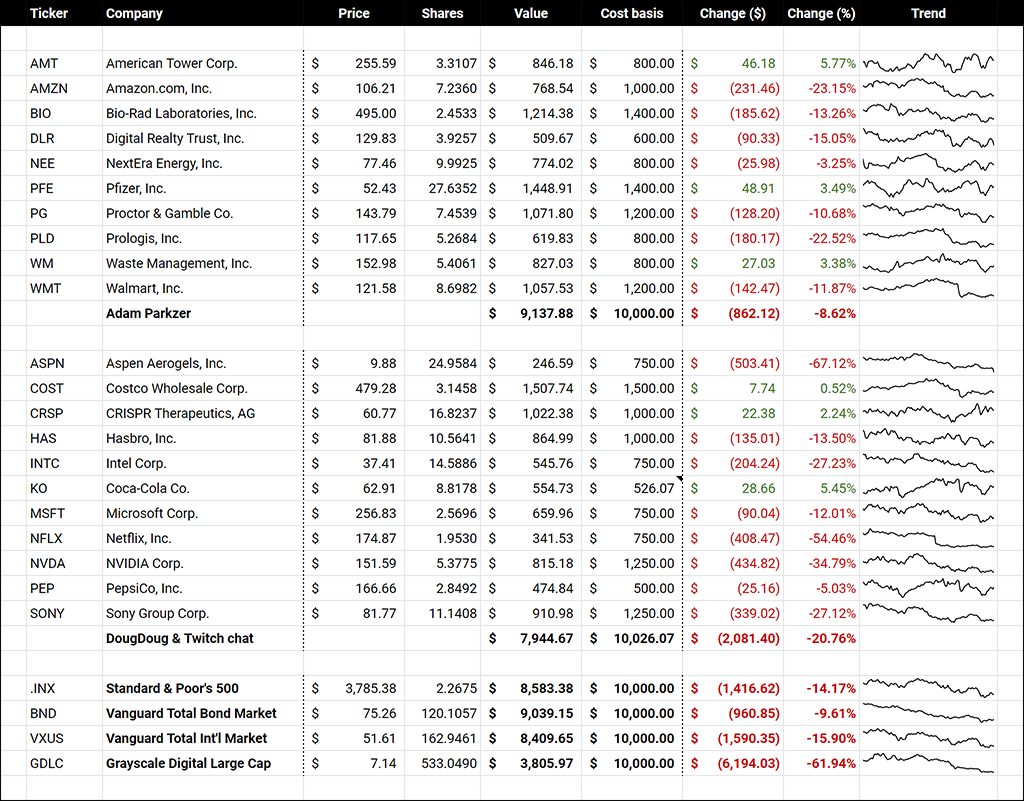

As promised, to wrap up, here is a breakdown of how my $10,000 stock investing challenge with Doug Wreden is going:

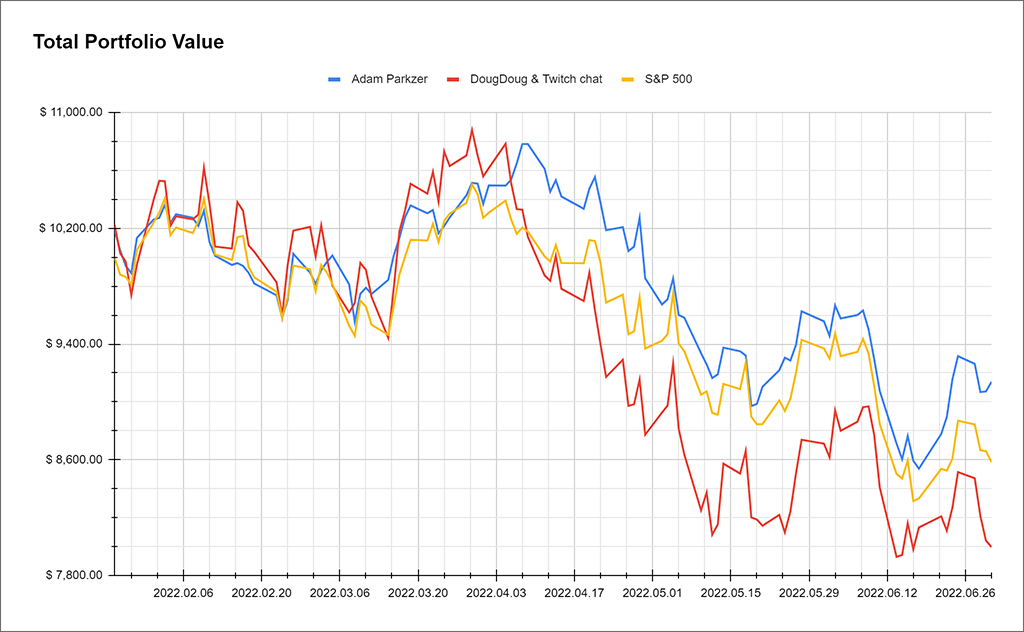

My portfolio is weathering the stock market decline relatively well with a balance of $9,137.88, managing not only to beat Doug and his Twitch chat’s portfolio, but also the S&P 500 and even the bond market. Doug’s portfolio is at $7,944.67, rapidly re-approaching its all-time low. However, if it’s any consolation, I guess he and his community can at least be happy that they didn’t go all-in on cryptocurrency, which would be down to $3,805.97 by now.