Disclaimer: I am not a registered investment advisor, and even if I was, I wouldn’t be your investment advisor. The information found in this blog post is intended to be strictly anecdotal and should not be construed as financial advice. Everyone’s situation is uniquely different and requires personalized attention, so if you are seeking guidance, be sure to consult a licensed and certified professional.

With the final few days of 2022 falling on a weekend and the last trading day of the year having already closed yesterday, I decided to do my quarterly investment allocation breakdown a day earlier than I usually do, as my final blog post of 2022.

As prerequisite reading, I highly recommend my investment allocation breakdowns for the second and third quarters of 2022 in order to get appropriate context for this post.

Cash It might seem like I can’t decide what I want to do with my cash, considering that I was hoarding it during the market instability, then dumped all of it into the stock market last quarter, before now hoarding cash once again. There are two reasons why I kept more of my money in cash this quarter:

| 8.14% |

Domestic broad market index funds Of my holdings in domestic broad market index funds, 45.95% of it is in high-yield dividend funds and the other 54.05% is in a total stock market fund. I have a feeling that the market still isn’t done doing some unexpected things, so until then, I’ll probably be putting more in dividend funds as a hedge against the volatility, and then hopefully get lucky with the timing and move it over into growth funds before a bulk of the market recovery happens. If not, then at least I was still in the market farming dividends. | 42.87% |

International total market index funds | 4.46% |

Target date funds Out of my target date funds, 51.31% is allocated towards a retirement year of 2055 and 40.42% is allocated towards a retirement year of 2060. Keep in mind that this does not mean that I actually plan on retiring on or around those years. This is merely a simplified indicator of the degree of risk I’m willing to take with my portfolio, i.e., by 2055-2060ish, I want 100% of this money in bonds, money market funds, or cash-equivalents to ensure I do not suddenly lose a lot of value to a volatile market. The remaining 8.27% is targeted towards other dates of stability and are not necessarily retirement-related. | 17.15% |

Real estate investment trusts (REITs) | 13.96% |

Bonds | 5.55% |

Cryptocurrency Still holding… | 1.32% |

Individual stocks and private companies As a reminder, the $10,000 investing challenge with Doug Wreden (about which I will give an update at the end of this blog post) is not included in this section, as I didn’t want to risk giving out any clues that would allow people to potentially reverse engineer my net worth based on these percentages. | 3.97% |

Precious metals | 1.03% |

Fine art, and other collectibles | 1.55% |

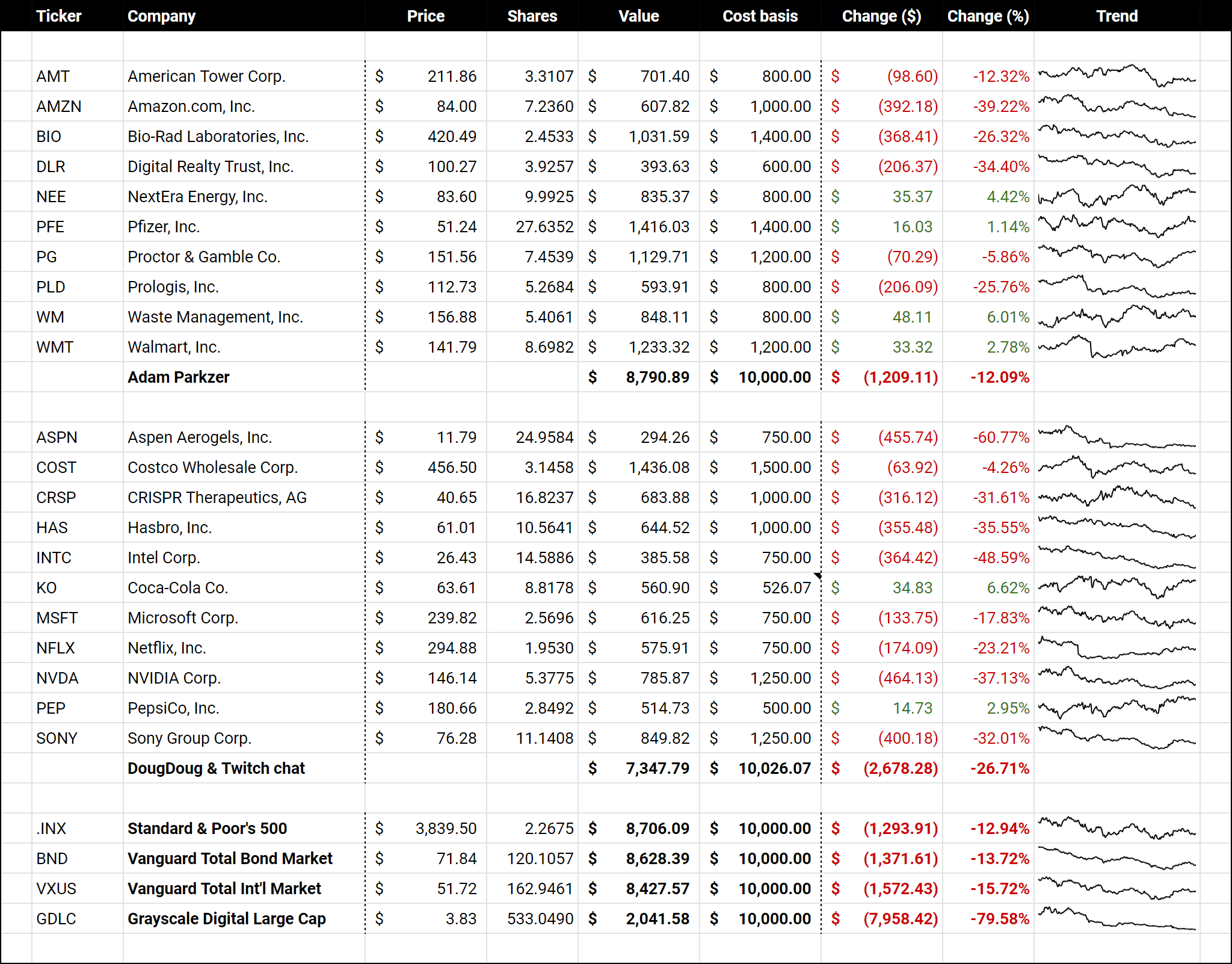

A little over 11 months ago, my friend Doug Wreden and I did a stock market investing challenge where we both put US$10k into individual companies to see whose portfolio would be ahead after one year. Doug relied heavily on his Twitch chat to make the decisions, while I made all my decisions on my own.

Here is a table showing the current state of our holdings, as well as a few benchmarks at the bottom:

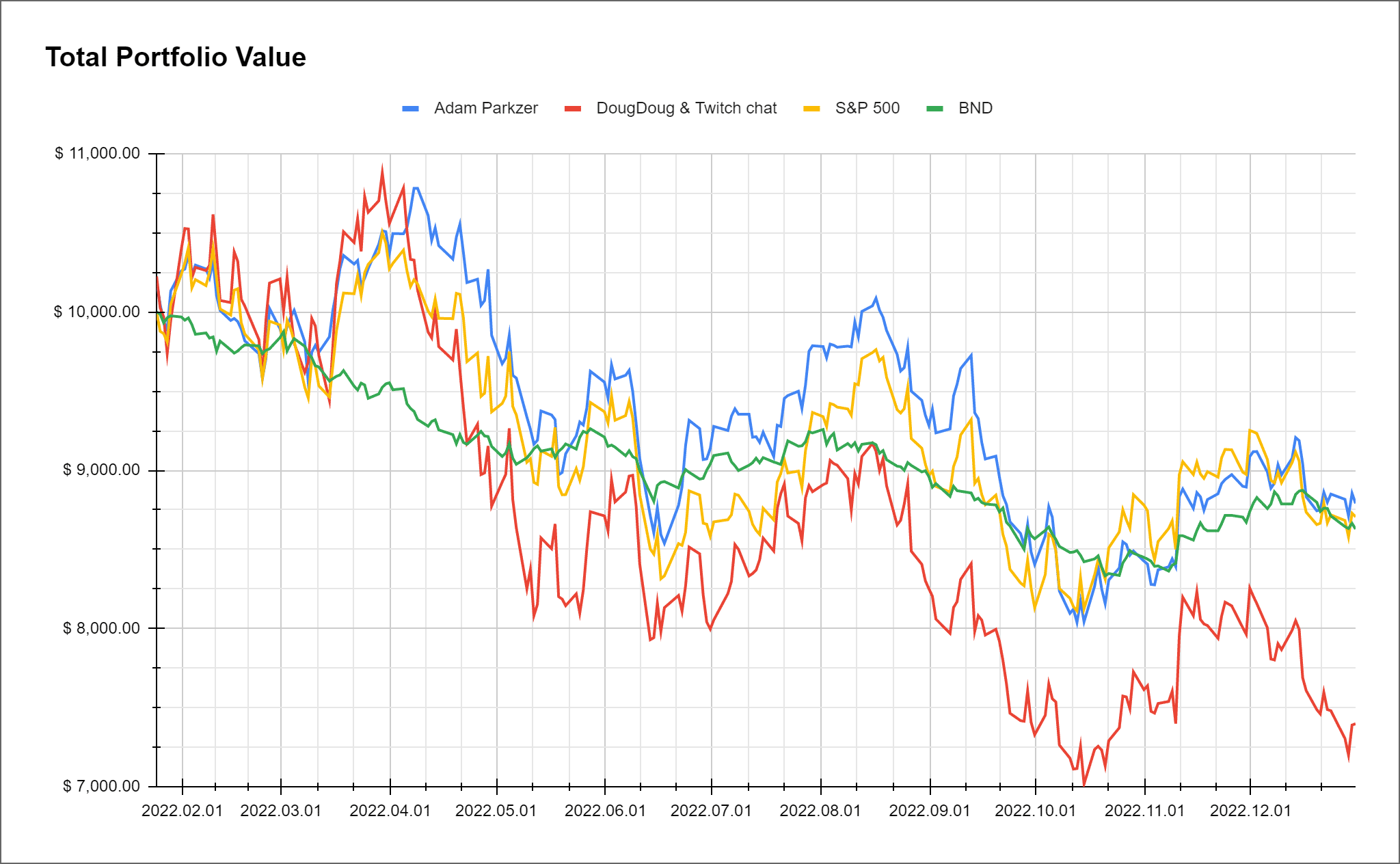

Here is a graph of the total value of Doug’s and my portfolios, alongside what our portfolio value would have been had we invested the full amount in the S&P 500 or the total bond market instead:

My portfolio was built specifically to weather a stock market decline, and it is clearly serving its purpose, as I’ve had a solid lead over Doug since early April. With that being said, anything can still happen, and if there is a huge rally at the beginning of 2023 that causes tech stocks to spike in price again like it did during the pandemic, it is not impossible for Doug to just barely squeeze out a win right at the finish.