Disclaimer: I am not a registered investment advisor, nor do I have the intent or proper qualifications to become one. The information contained in this blog post is strictly anecdotal and should not be construed as financial advice. Everyone’s situation is uniquely different, so if you need guidance with your own financial strategy, consult a certified professional.

Last quarter, I published a comprehensive breakdown and explanation of my investment allocation as of 2022 Q2. If you want the proper context to this blog post, you should review that post first as prerequisite reading.

Cash Literal days after publishing my previous investment allocation breakdown, I dumped a majority of my cash back into the stock market. In essence, I was doing the precise thing that like to tell everyone not to do, and that is, timing the market. Thus, I am down to a minuscule amount of cash left in my checking and savings accounts. | 1.57% |

Domestic broad market index funds Building on what I just mentioned about dumping cash back into the stock market… At first, I thought my timing was great—I held cash throughout a majority of 2022 Q2 when the S&P 500 peaked at about $4,582.64 and generally stayed above $4,000 throughout the whole quarter. Right as it dropped to ~$3,800 towards the beginning of July, I bought back in aggressively. The S&P 500 continued to rise to a high of a closing price of $4,305.20 on August 16, and I was satisfied. Then, of course, the market started falling again. I did not pull my money back out into cash and continued holding. As of market close on September 30, the S&P 500 is at $3,585.62, lower than my aggressive buy-back price. For now, I’m still satisfied with the fact that I bought back in at ~$3,800 and not between $4,000-4,500. I have absolutely no substantive idea what’s going to happen to the stock market from now on, so unless I pick up on some obvious clues, I’m going to hold steady and continue dollar-cost averaging until I have a better plan. | 43.20% |

International total market index funds The international market hasn’t been doing very well, and with China’s current economic crisis, it may be worth it to try and do a bit of optimization by withdrawing from the international market temporarily. This would be a great opportunity for some tax loss harvesting, so I may be doing some calculations and putting in some transactions soon. | 4.53% |

Target date funds Like usual, there is going to be next to no change in target date funds in Q3 and Q4, as I usually contribute a maximum amount as soon as possible in the beginning of the year in Q1, and then again during tax due date season in Q2 when I know my new SEP-IRA contribution limit. Consequently, the percentage will remain fairly consistent and decline slowly, caused by the rest of my net worth increasing but me being unable to contribute more to retirement funds until the following calendar year. | 18.39% |

Real estate investment trusts (REITs) With the real estate market stabilizing again after the post-pandemic surge, and with my home city of Las Vegas being one of the top fastest-cooling real estate markets in the United States of America, I’m keeping an eye out on physical real estate to make sure I don’t miss out on some great opportunities. However, until I find one, I will be keeping my real estate investments in REITs. | 15.60% |

Bonds Usually, bonds are pretty boring, but now that interest rates are rising, bonds are becoming a lot more interesting because of how they tell a story about interest rates and exemplify a core principle of investing. Regardless, I haven’t made any changes with regards to my bond holdings. | 6.47% |

Cryptocurrency Since the beginning of the previous quarter, Bitcoin has been relatively even in price, but because I’m invested in broader cryptocurrency indexes and not just a single coin, my overall cryptocurrency portfolio has actually gone up in value. Regardless, I’ve lost significantly more than two-thirds of my original investment, so overall, cryptocurrency has not been very kind to me. | 2.96% |

Individual stocks and private companies As a reminder, the $10,000 investing challenge with Doug Wreden (about which I will give an update at the end of this blog post) is not included in this section, as I didn’t want people to be able to have any clues to potentially reverse engineer my net worth based on these percentages. | 4.47% |

Precious metals I put a little bit of money into gold and other precious metals during market instability because I thought it would be a good way to diversify into something that has historically been a more reliable store of value during recessions, but apparently, either I was horribly wrong or my timing was horribly bad. I’ve lost over a third of my original investment, but because my commitment is such a small amount, I just plan on holding. | 1.00% |

Fine art, and other collectibles I sort of suffered the same fate in this category as many other investors. Back when collecting investment-grade Pokémon cards was the hype thing to do, many people obsessively bought packs and cleared store shelves of new releases, depriving actual children from buying them to play with for fun. After a while, that craze settled, and people slowly lost interest. When I first started looking for fine art investments, it consumed hours of my time because I was so intrinsically interested in and intrigued by this concept that was new to me. However, after the dust settled, it ended up just being another form of diversification. I plan on keeping this class of investment in my portfolio for a long time, but as of this past quarter, I haven’t been actively trading or doing additional research. | 1.81% |

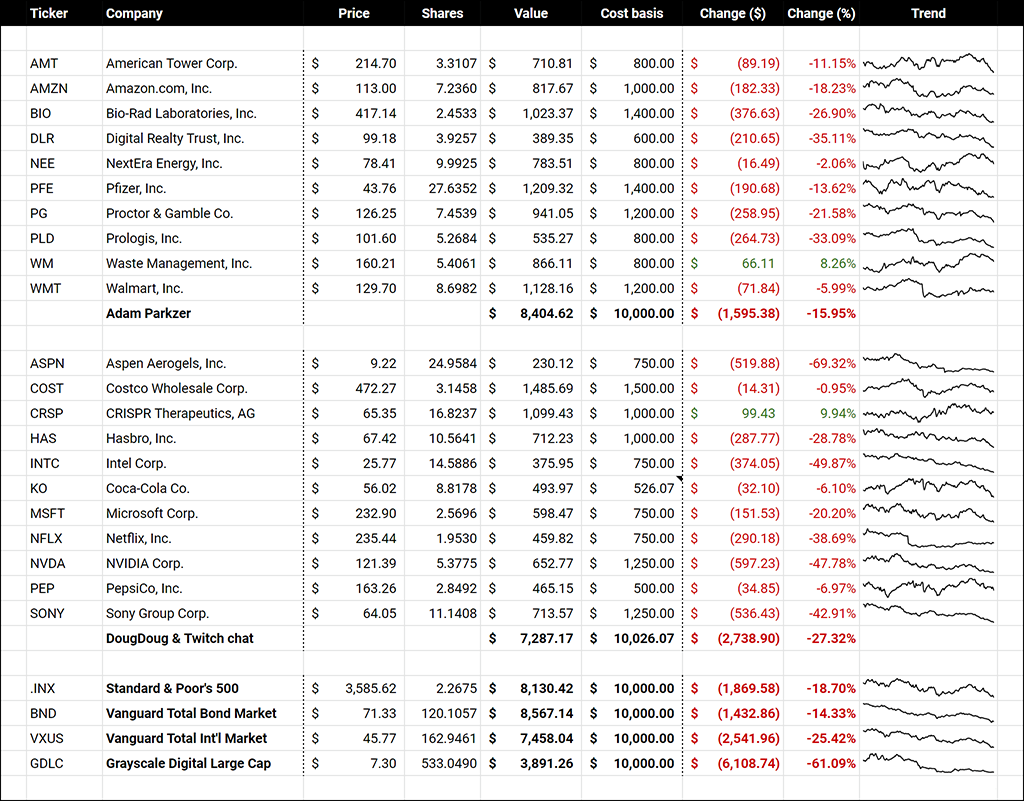

And now, the part that, for some of you, is the only reason why you come to these quarterly investment breakdowns… here is the current state of my $10,000 investing challenge with Doug Wreden. If you’re not sure what this is, you can read the aforelinked blog post for a comprehensive explanation.

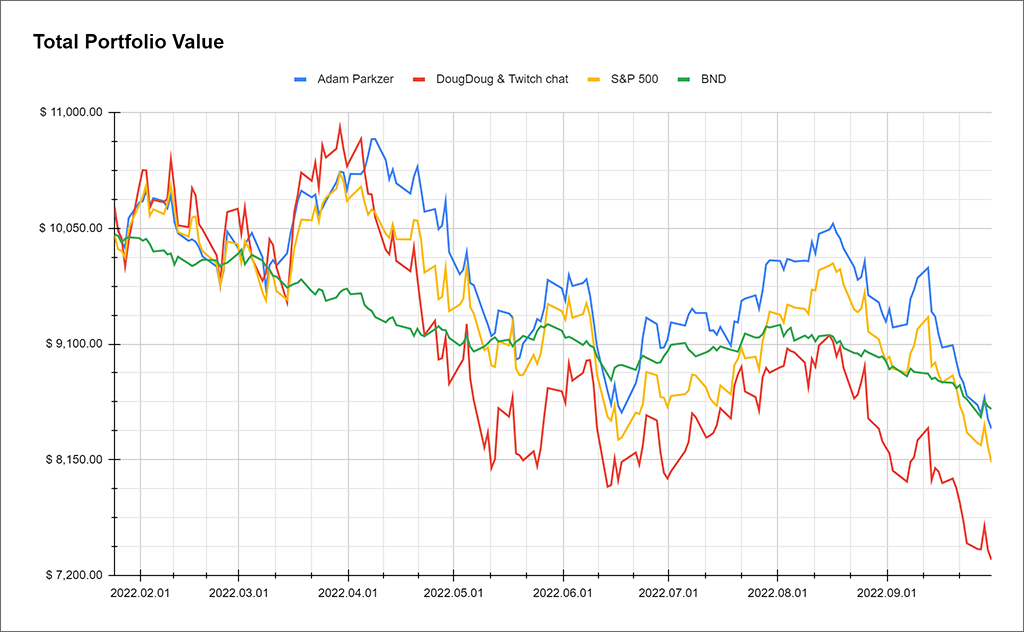

As of market close on September 30, 2022, my portfolio is worth $8,404.62 and Doug’s portfolio is worth $7,287.17. I’ve maintained my lead over the S&P 500, while Doug is avoiding last place only thanks to the crashed cryptocurrency market.

One notable change this quarter is that the bond market managed to just barely squeeze past me. I’ve only temporarily been behind the bond market during the harshest stock market dips, so it’s very possible that I’ll be winning again in a few more days, but if the market continues to decline, this can be a decent demonstration of the relative stability of bonds.

Because of this, I decided to add the Vanguard Total Bond Market Index Fund to the chart.

Doug’s portfolio managed to reach a new all-time low, and compared to last quarter’s chart, I actually had to adjust the bottom of the y-axis from $7,800 to $7,200 to fit him in.

We’re 115 days away from the end of the 1-year mark, which means we have a little less than a third of the challenge duration remaining. Regardless, that’s still a long time, and if the current chart is any indication, anything can happen over the next four months.